XLM Insight | Stellar Lumens News, Price Trends & Guides

XLM Insight | Stellar Lumens News, Price Trends & Guides

For decades, we’ve been told a story about the internet—that it was a tool for connection, a global library, a digital town square. And it was. But that was just the prologue. We’re now living through the first chapter of its real purpose: the seamless, native integration of value and ownership into the fabric of our digital lives.

I’m not talking about some far-off, abstract future. I’m talking about something that’s happening right now, quietly, inside an app you probably use every day. Imagine if your bank wasn't a cold, separate institution you had to visit, but a living, breathing part of your most-used social network. Imagine if you weren't just a customer, but an owner. This isn't a thought experiment anymore. It’s the reality being built by a project called EVAA Protocol on The Open Network (TON), and it’s happening entirely within Telegram.

When I first read the announcement, TON Protocol EVAA Announces Transition to Decentralized Governance, I honestly just sat back in my chair, speechless. It’s one of those moments that reminds me why I got into this field in the first place. This is the kind of paradigm shift that doesn’t just change an industry; it redefines our relationship with technology itself.

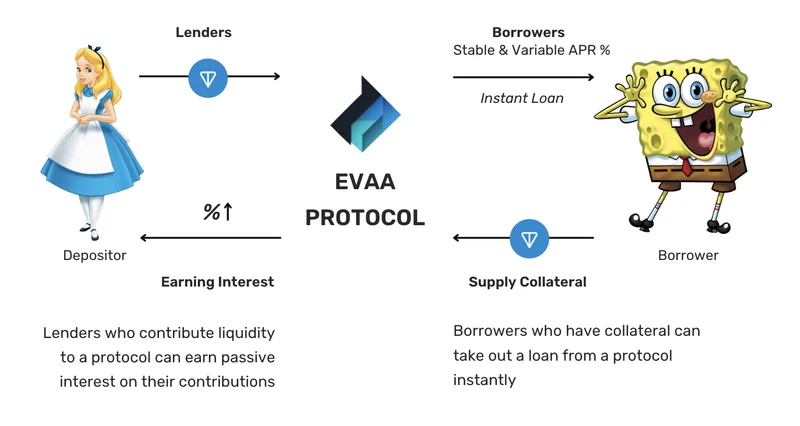

Let’s be honest for a moment. For all its revolutionary promise, decentralized finance, or DeFi, has been a bit of a gated community. It’s powerful, yes, but it often requires a Ph.D. in jargon, a collection of browser extensions, and the patience of a saint to navigate its clunky interfaces. It’s a world built by engineers, for engineers. That friction has been the single biggest barrier to mass adoption.

What EVAA has done is nothing short of brilliant. They didn’t try to build a better front door to the world of DeFi; they built DeFi directly into a room a billion people already live in. The entire protocol operates as a Telegram Mini App—in simpler terms, it’s a full-fledged financial application that runs inside your chat window, no downloads or separate wallets required. You can lend, borrow, and earn yield on your assets with the same ease as sending a sticker.

This isn’t some niche prototype. The numbers are staggering. The protocol has already processed over $1.4 billion in transactions and onboarded 300,000 wallets. Think about that. This isn't just a proof-of-concept; it's a functioning, scaled financial engine humming away inside a messenger app. It’s a testament to a simple, profound truth: the most powerful technology is the technology that disappears.

Where does this lead? What happens when financial tools become as intuitive and accessible as a conversation? This is the question that should keep every traditional banker awake at night.

The real breakthrough here, the part that truly ignites the imagination, is what comes next. EVAA isn’t content with just being an app; it’s becoming an economy. With the launch of its EVAA token and the transition to a Decentralized Autonomous Organization (DAO), the project is handing the keys over to its users.

This is a fundamental shift in the power dynamic. It’s like the difference between renting an apartment and owning the building. As a renter, you’re just a user. As an owner, you have a say in the rules, you share in the success, and you are invested in the community’s future. The EVAA token isn't just a digital asset; it's a vote, a share in the protocol's revenue, and a key to enhanced services. Holders will decide on everything from risk parameters to fee structures.

This is the kind of thing that could spark a Cambrian explosion of innovation—imagine a billion-person user base suddenly empowered not just to use their financial infrastructure but to co-own and co-create it, shaping its future in real-time based on their collective needs. This isn’t just a new feature; it's a new form of digital citizenship. Of course, this introduces a new layer of responsibility. A community-run protocol must be vigilant, educated, and engaged to steer the ship correctly. But is that risk not worth the monumental reward of true digital sovereignty?

I see this as being analogous to the invention of the printing press. Before Gutenberg, information was controlled by a select few. Afterward, it was in the hands of the many, unleashing centuries of progress. We are on the cusp of a similar moment for finance.

The team’s vision extends far beyond simple lending. CEO Vlad Kamyshov said it best: “We are creating a liquidity layer for Telegram where you can earn income, borrow and spend — all in one place.” They’re planning to enable crypto spending on everyday purchases through traditional payment cards, right from Telegram. They’re exploring using social reputation—your digital identity and connections—to reduce collateral requirements for loans.

What happens when your trustworthiness within your community has tangible financial value? What new forms of commerce and collaboration become possible when the line between our social and financial lives completely dissolves? This isn't just about making finance easier. It's about making it more human.

For the last two decades, the story of technology was one of unbundling. Music was unbundled from albums, news from newspapers, and friends from physical locations. We’ve been living in a fragmented digital world. What we're witnessing with projects like EVAA is the start of a powerful and profound rebundling.

This isn’t just bolting a payment feature onto a social app. This is weaving the very concept of ownership, governance, and financial utility into the core of our primary communication platform. The wall between the "social graph" and the "financial graph" is crumbling, and what will emerge from the dust is a unified digital life where our identity, our community, and our assets are all part of the same seamless experience. The bank of the future isn't a building or even a standalone app. It's a conversation. And we're all about to become its shareholders.